This Week in Disasters

Source: Aftermath of Hawaii earthquake. Source: County of Hawai'i

Plus: Why wildfire prevention is planned work, not emergency work

Welcome back to This Week in Disasters! This newsletter combines expert perspectives with a weekly roundup of upcoming threats, recent natural disasters, and available survivor assistance. If you’re a Risk, Insurance, Employee Assistance, NGO or Emergency Management professional (or you’re just really curious about disasters in the United States!) you’re in the right place.

Major Disasters of the Last Week

A magnitude 6.0 earthquake struck South Kona at 9:46 PM HST Friday, damaging homes, knocking out power to 1,000 customers, and closing West Hawaii roads with rockslides. It is the second damaging event to hit Hawaii in ten weeks, following the March Kona Low storms. Read more. |

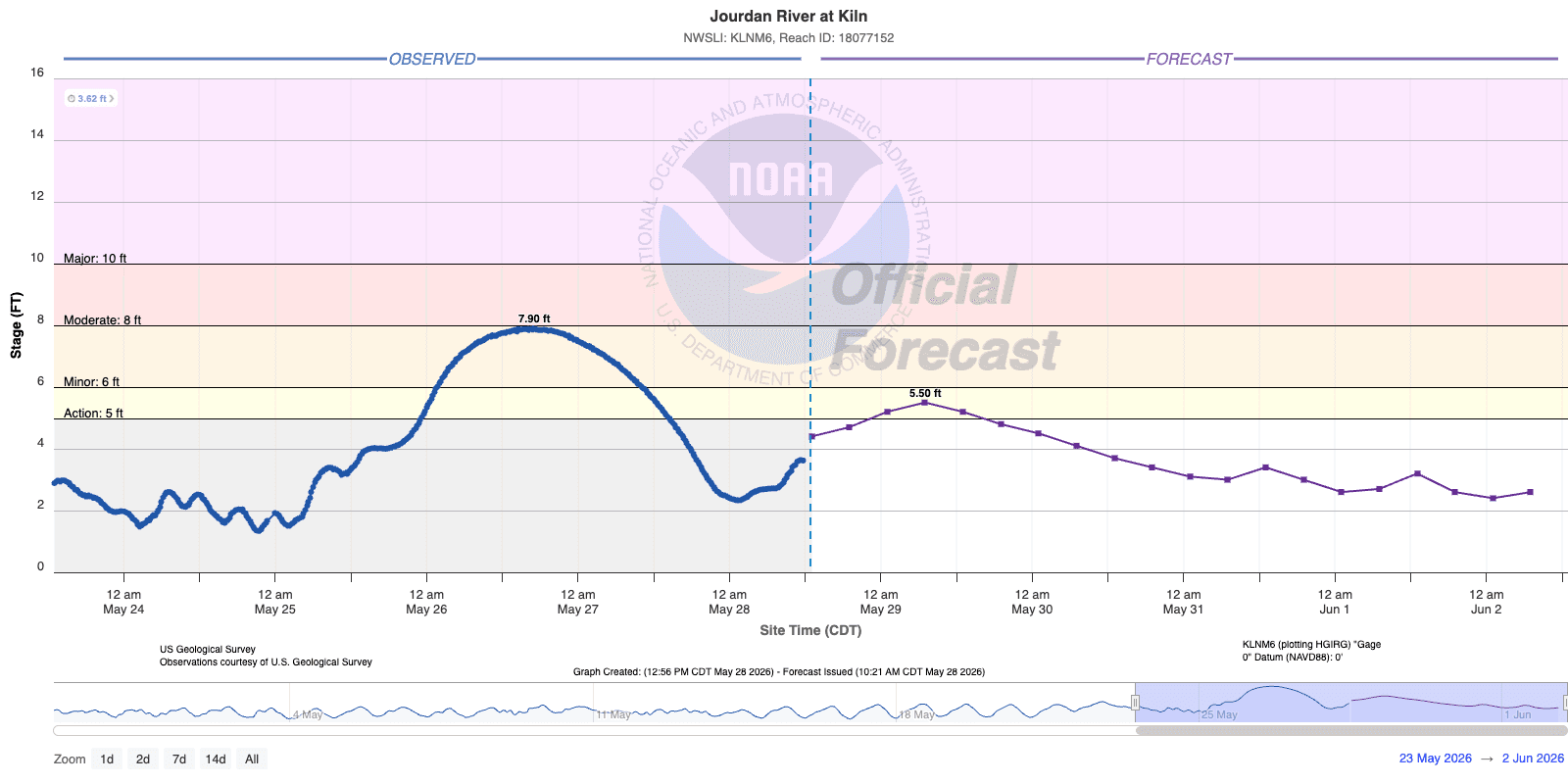

Six to 12 inches of rain sent the Jourdan River 6 to 7 feet above normal, cutting off the 100-home Jourdan River Shores subdivision near Kiln and prompting boat evacuations. Floodwater reached knee-deep on streets in Picayune as the Pearl River crested 8 inches above flood stage, with active flood warnings continuing across the Pine Belt as the Leaf and Chickasawhay rivers rise. Read more. |

A multi-day outbreak from the Texas Panhandle to the Florida coast between May 22 and May 25 produced confirmed tornadoes in Texas, Alabama, and Florida along with widespread flash flooding, hail, and damaging winds. A tornado skipped across Houston and Henry counties in Alabama the evening of May 25, destroying one home along Highway 15 and tearing the roof off the WDHN news station during live storm coverage. Read more. |

Forecasted Risks for Next Week

Heavy rain and flash flood potential across the southern Plains. A stalling front targets the Hill Country, eastern Oklahoma, and Arkansas with additional severe weather and heavy rainfall chances into next week.

Hawaii aftershock watch. USGS expects continued aftershocks from the May 22 magnitude 6.0 earthquake for days to weeks, with the possibility, though low, of a stronger followup quake.

Source: NOAA

Disasters in the Headlines

Wildfire season is off to a historic start and it could get worse

These states are bracing for a home insurance surge ahead of hurricane season

The 'C' in culture and crisis planning

A FEMA Insider Says Morale Has Never Been Lower at the Embattled Agency

Top FEMA official Bob Fenton says 'we're ready for hurricane season

PRO PERSPECTIVE

When the Smoke Comes, the Money Can't Help

During the Palisades fires, a homeowner reached out to Allied Disaster Defense with an offer most contractors would dream about. "I have a blank check for you," he told the team. "If you can get to my address, I'll pay you whatever you need. I just need you to spray retardant and prepare my home."

They could not reach him. The roads were closed.

"Most homeowners say, I'll just deal with it when it happens and I'll just pay more money," O.P. Almaraz said, reflecting on the call months later. "Well, okay, that's one aspect of it. But if people can't get to you, your money doesn't help."

The lesson sits inside the story. Once an event is underway, no amount of money summons a crew that cannot physically reach the property. Prevention is calendar work, not emergency work, and Almaraz has spent thirty years watching homeowners discover that distinction at the worst possible moment.

Built in Both Halves of the Cycle

Almaraz is the founder of Allied Disaster Defense, the Southern California firm he launched in 2021 around home hardening and wildfire prevention. He came to the work the long way around. He started as a carpet installer at 22, eventually got a foothold at ServiceMaster, and over the next 30 years moved through every layer of the restoration industry. "You have a homeowner that's in pain, that has a claim, and you have the insurance company that has the money," he said. "I became the bridge to help the homeowner get what they needed, and the insurance company pays what's fair. After a certain amount of time, it became magic. I was like, this is my world."

When his own neighborhood was put under voluntary evacuation in 2022, the pivot turned personal. He partnered with the Insurance Institute for Business and Home Safety (IBHS) to help refine the Wildfire Prepared Home (WPH) criteria. "I'm willing to help you and I'm willing to be the guinea pig," he told them, and turned his own property into a test case. It became the first WPH+ designated home in Southern California. His team now includes 12 former firefighters who assess properties the way fire behaves. "They're looking at it from a wildfire perspective," Almaraz said. "Here's the hillside. The wildfire is gonna run up three times as fast as it normally would if we have a different topography."

The biographical detail matters more than it first appears. Almaraz did not arrive at prevention through policy work, actuarial modeling, or a consulting practice. He arrived through three decades of standing inside damaged homes with homeowners in the worst week of their lives. That vantage point produces a different kind of expertise than the resilience conversation is usually built around.

The Timeline Mismatch is Structural, Not Anecdotal

The most uncomfortable observation in the conversation is about restoration timelines, and Almaraz frames it as an expectations problem before it ever becomes a billing problem. "The expectation of the recovery of that damage is not the truth in their mind," he said of homeowners after a fire. The disconnect compounds when adjusters share that gap.

He recounted a Palisades-era walkthrough with an adjuster who estimated three months to restore a smoke-damaged home that was still standing. Almaraz, looking at the mechanical work, the special-order window, the attic insulation, the testing, and the deodorization, said six.

"OP, that's ridiculous," the adjuster said, in front of the homeowner. Nine months later, the homeowner still was not back in the house. "Even sometimes the insurance adjusters don't really understand what it takes," Almaraz said.

The interesting part is not the disagreement. It is that the gap is predictable. Adjusters reason from claim playbooks. Contractors reason from supply chains. A six-week window special-order timeline is already baked into the schedule before anyone opens a file. When that information asymmetry sits between the insurer's promise and the homeowner's expectation, every additional week of displacement, every disrupted school commute, every strained marriage gets absorbed silently by trust in the carrier. The structure assigns the blame to the contractor and the cost to the policyholder, but the leak is upstream.

There is a clear operational lever here, and almost nobody is pulling it. Field intelligence from contractors needs to flow back into adjuster training before the next event, not after the next complaint. The downstream cost is also not measured in repair budgets. "We have life interruptions that take place," Almaraz said. "Now you're taking a different route to get the kids to school. You're relocated. Things get out of whack. There's a new normal taking place where everyone in the family is trying to accommodate everyone else's new needs. I've seen a lot of relationships suffer." That is what is being underwritten when a timeline is wrong.

Aesthetic Resistance Is a Missing Market, Not a Mindset

Almaraz is blunt about why prevention adoption lags. "Prevention is not attractive. It's not sexy. People don't want to do it." But the obstacle he hits most often is more specific than apathy. Homeowners will replace vents, upgrade siding, even install automatic water shutoffs. They stall when asked to remove a 20-foot Italian Cypress that doubles as a fire wick along the front of the house. "They burn so hot that it's like a candle," he said. "As soon as that goes, the house is ignited. And that's where they say, this is too much for me. It's really the aesthetics."

The standard interpretation is homeowner irrationality. Almaraz's reading is sharper and more useful. The aesthetic barrier is a coordination failure, not a behavioral one. There is no professional class trained, marketed, and priced to redesign residential landscapes for fire adaptation at scale, the way kitchen designers exist for renovations. "Landscape architects really need to jump on board and help people see a different vision," Almaraz said. "Help them see that once this comes off, all hope is not lost. Look at how beautiful this can look."

He pointed to Berkeley's Zone 0 work, where designers are being brought in to help homeowners visualize fire-adapted yards, as the kind of cross-discipline move the field needs more of. For emergency managers and resilience offices funding outreach, the implication is direct. Vegetation mandates without paired visualization support are policies designed to be slow.

The Three Moves That Beat Most of the Policy Debate

Asked what a homeowner should do before they call any professional, Almaraz pushes back on his own value proposition first. "You don't need me. I promise you don't need me. There is so much DIY work you can do." His prioritized list maps closely to the IBHS field data:

Ember resistant vents first. "It's not the wall of flames you're fighting. It's the embers. Those are going to get to you first. The ember attack is what we're trying to prevent." Off-the-shelf replacements from Brand Guard and others are installable without a contractor.

Zone 0 vegetation management second. Nothing combustible within the first five feet of the structure. Cushions, doormats, plastic trash cans, and patio rugs come inside or move away before evacuation.

Fire retardant pre-treatment for properties with significant hillside vegetation. Almaraz's team documented a Malibu fire line stopping at the treated edge. "You could see within six inches the actual fire turned itself off."

None of these require legislation, premium subsidy, or a contractor in the driveway. For professionals shaping outreach campaigns, the lesson is that the highest-leverage advice is also the simplest, and it is still not the default message reaching homeowners.

The Question That Belongs in Every Annual Plan

The story Almaraz keeps returning to is the one that ends in silence. The blank check community from the Palisades response, called back months later with open roads and clear calendars, went quiet. "As much as I would love to be hopeful," he said, "I'm like, darn it, what is it gonna take?"

That is the question worth carrying into the next planning cycle. The willingness to pay is not the constraint. The willingness to act before the smoke is, and the systems built around prevention, from carrier incentives to landscape design to adjuster training, have not yet caught up with what the field already knows.

Active Federal Major Disasters

There is usually a 60 day window to apply for help after a disaster is declared. The following disasters are still actively taking applications from survivors for financial support.

The following disasters are actively taking applications from survivors for financial support. To apply, survivors can visit DisasterAssistance.gov or call the FEMA Helpline at 1-800‑621‑3362.

Mississippi - Severe Winter StormSTATUS Major Disaster declared February 6, 2026; IA applications accepted in eligible counties until June 10, 2026. AFFECTED COUNTIES Adams, Alcorn, Attala, Benton, Bolivar, Calhoun, Carroll, Claiborne, Coahoma, DeSoto, Grenada, Holmes, Humphreys, Issaquena, Jefferson, Lafayette, Lee, Leflore, Marshall, Mississippi Choctaw Indian Reservation, Montgomery, Panola, Pontotoc, Prentiss, Quitman, Sharkey, Sunflower, Tallahatchie, Tate, Tippah, Tishomingo, Tunica, Union, Warren, Washington, Yalobusha, Yazoo |

Tennessee - Severe Winter StormSTATUS Major Disaster declared February 6, 2026; IA applications accepted in eligible counties until June 10, 2026. AFFECTED COUNTIES Benton, Carroll, Cheatham, Chester, Clay, Davidson, Decatur, Dickson, Dyer, Fayette, Hardeman, Hardin, Henderson, Hickman, Lewis, Macon, Madison, Maury, McNairy, Montgomery, Perry, Robertson, Rutherford, Shelby, Sumner, Trousdale, Wayne, Williamson, Wilson |

Washington - Severe Storms, Straight-line Winds, Flooding, Landslides, and MudslidesSTATUS Major Disaster declared April 7, 2026; IA applications accepted in eligible counties until June 10, 2026. AFFECTED COUNTIES Chehalis Indian Reservation, Chelan, Grays Harbor, King, Lewis, Lummi Indian Reservation, Muckleshoot Indian Reservation, Nisqually Indian Reservation, Nooksack Indian Reservation, Pacific, Pierce, Puyallup Indian Reservation, Quinault Indian Reservation, Samish (TDSA), Sauk-Suiattle Indian Reservation, Shoalwater Bay Reservation, Skagit, Snohomish, Squaxin Island Indian Reservation, Stillaguamish Indian Reservation, Swinomish Indian Reservation, Thurston, Tulalip Indian Reservation, Upper Skagit Indian Reservation, Whatcom |

Hawaii - Kona Low Weather SystemsSTATUS Major Disaster declared April 7, 2026; IA applications accepted in eligible counties until June 14, 2026. AFFECTED COUNTIES Hawaii, Honolulu, Maui |

[NEW] Commonwealth of the Northern Mariana Islands - Super Typhoon SinlakuSTATUS Major Disaster declared April 23, 2026; IA applications accepted in eligible counties until June 22, 2026. AFFECTED COUNTIES Northern Islands, Rota, Saipan, Tinian |

North Carolina - Flooding and Storm Damage from Tropical Storm ChantalSTATUS SBA disaster declaration approved July 26, 2025; applications open for residents and businesses in eight NC counties. The deadline to return economic injury applications has been extended to September 30, 2026. APPLY NOW AFFECTED COUNTIES Alamance, Caswell, Chatham, Durham, Granville, Orange, Person, Wake Counties |

Sign up for This Week in Disasters here.